_AZ_Initial.png)

YOUR CHECKLIST FOR ENROLLING IN MEDICARE

- Michael Braden

- May 18

- 13 min read

Michael T. Braden April 29, 2026 MEDICARE ENROLLMENT

YOUR MEDICARE ENROLLMENT CHECKLIST

If you miss a deadline by a few weeks, you could face a permanent penalty on your monthly medicare premiums. Making assumptions without checking can force you to choose a new doctor(s). Not reading the fine print may mean you lack coverage outside your county, but worst of all, if you do not fully understand your options when you turn 65, your decisions can cause financial distress and a catastrophe that some may never recover from. But all of these issues can easily be avoided if you know the right steps to take and follow the outline in this article.

The good news is that this process becomes manageable when you follow a clear sequence of steps. Our goal for everyone reading this article is to have a clearer, better understanding of the Medicare Enrollment Process, and the knowledge and confidence to set you and your family up for success, knowing your healthcare choices are in place for the next 20-25 years. Or the Medicare Enrollment Checklist will guide you through the Medicare Maze step by step, and make sure that you completely understand each of your decisions.

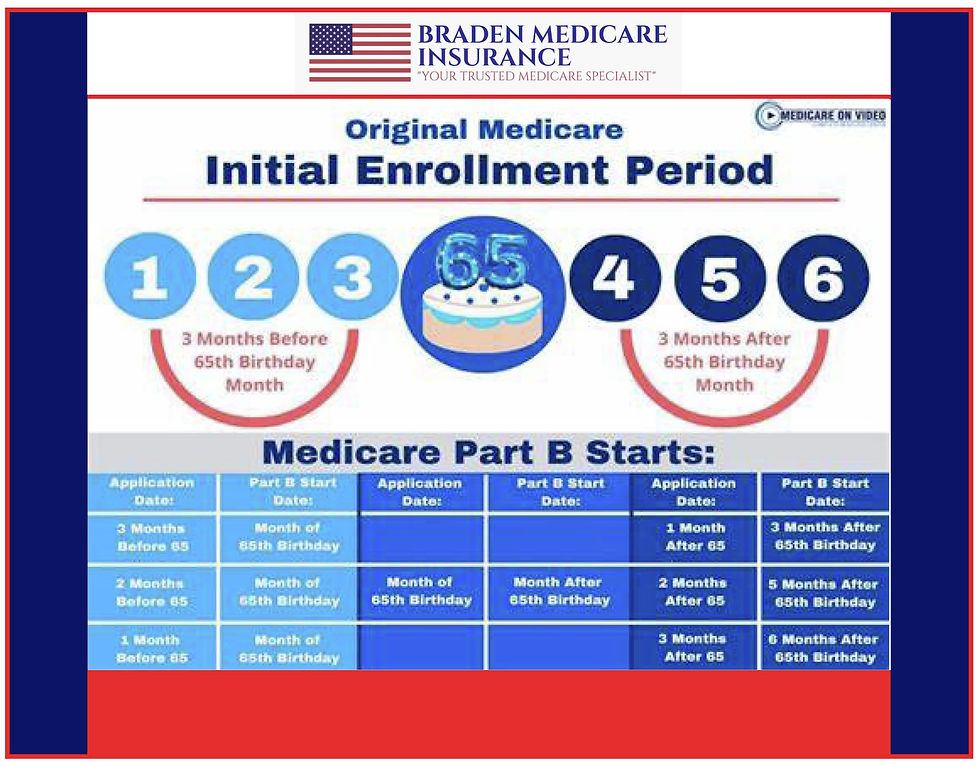

Everyone has a 7-month Initial Enrollment Period that starts 3 months before the month when you turn 65. This is the first major thing you need to remember and to get right, in order to avoid potential Medicare Part B and Medicare Part D penalties that could follow you for the rest of your life.

The next big decision is to choose the best healthcare plan for you and your family. You can choose to:

Enroll in Original Medicare.

Choose to enroll in Original Medicare and add a Medicare Supplement (Medigap) policy for additional protection.

Choose to enroll in a Medicare Advantage Plan (MA plans are often referred to as Medicare Part C or All-In-One plans).

Choosing between Original Medicare and Medicare Advantage is the biggest decision you will make, and it deserves to be taken seriously. I have seen far too many bad things happen to good people, and I do not want to see them happen to you. Healthcare decisions should be made based on your doctors, all of your medications being covered, where you can be seen and treated for your current and future medical needs, what is best for you and your family, and having a full understanding of premiums, budgets, co-pays, and co-insurance.

Included in your IEP (Initial Enrollment Period) is the Medicare Supplement Open Enrollment Period. This is a one-time only opportunity for you to join any Medicare Supplement/Medigap plan of your choosing, without having to divulge any health history, and you will have guaranteed acceptance, and insurance companies cannot deny your enrollment, regardless of your health history. Once your Medicare Supplement/Medigap Open Enrollment Period closes, that protection disappears forever.

LET'S TAKE A QUICK GLANCE AT THE STEPS YOU WILL BE TAKING

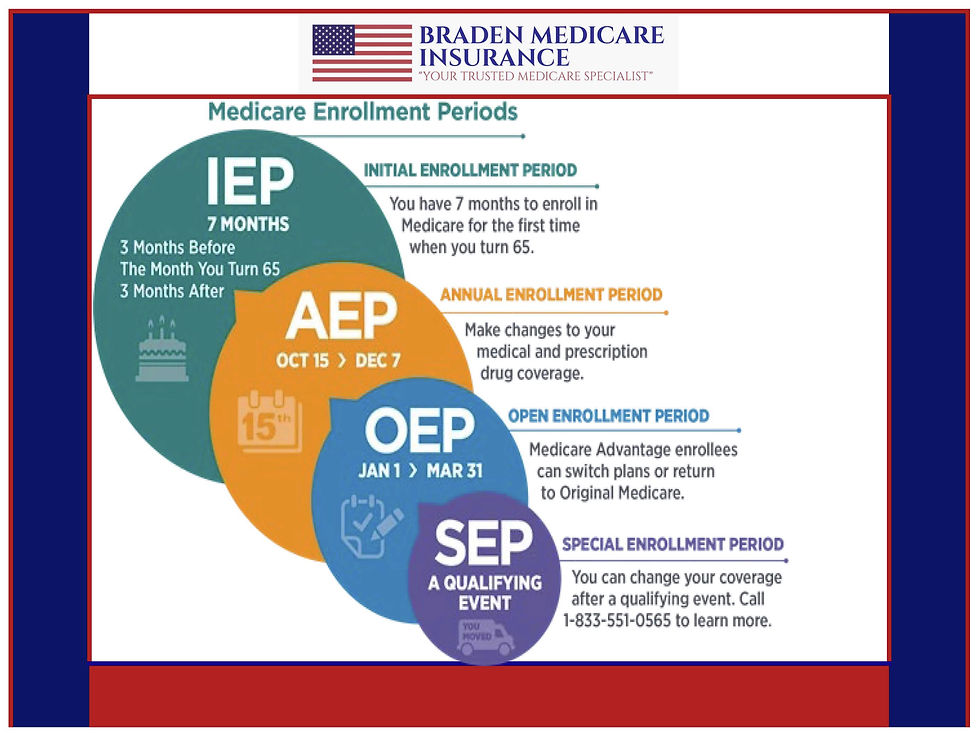

Step 1: Identify your Initial Enrollment Period (IEP), the 7-month window tied to your birthday.

Step 2: Choose your coverage path, Original Medicare or Medicare Advantage.

Step 3: Add prescription drug coverage (Part D) to avoid late penalties.

Step 4: Decide whether Medigap makes sense for you, and enroll during your protected window.

Step 5: Coordinate with any employer coverage or COBRA you currently have.

Step 6: Understand IRMAA surcharges and check for savings programs.

Step 7: Schedule an annual review every fall during the Annual Enrollment Period (AEP).

FAMILIARIZE YOURSELF WITH THE FOUR PARTS OF MEDICARE

#1 UNDERSTANDING YOUR IEP (INITIAL ENROLLMENT PERIOD)

Your Initial Enrollment Period (IEP) is the 7-month window around your 65th birthday when you can first enroll in Medicare Part A and Part B without penalty. Your Medicare Initial Enrollment Period spans 7 months total: the 3 months before your birthday month, your actual birthday month, and the 3 months after. That’s your primary window to sign up for Part A and Part B without facing penalties.

If you’re already receiving Social Security or Railroad Retirement Board benefits when you turn 65, you’ll be enrolled in Part A and Part B automatically. Your red, white, and blue Medicare card will arrive in the mail before your coverage starts. If you’re not yet receiving Social Security benefits, you’ll need to enroll actively through Social Security.

Timing matters even within the IEP. If you enroll during the first 3 months, coverage typically starts on the first day of your birthday month. If you enroll in months 4 through 7, your coverage start date is delayed. For someone who wants seamless coverage from day one, enrolling early in that window is the smarter move.

IF YOU MISS YOUR IEP WINDOW, THERE CAN BE CONSEQUENCES

Part B Late Enrollment Penalty: 10% added to your premium for every 12 months without coverage, permanently. For 2026, the Standard Part B Premium is $202.90 per month. Everyone who enrolls in Medicare is charged this monthly premium, regardless of whether you choose a Medicare Advantage plan or Original Medicare.

The Part B late enrollment penalty adds 10% to your premium for every 12-month period you went without coverage, and that surcharge stays with you permanently. The 2026 standard Part B premium is $202.90 per month, so even a one-year delay adds roughly $20 per month for life.

#2 THOUGHTFULLY EVALUATE YOUR COVERAGE NEEDS AND COMPARE ALL OPTIONS AVAILABLE TO YOU

Everyone must choose between Original Medicare (Parts A and B, often supplemented by Part D and most often by adding a Medicare Supplement Plan) or a Medicare Advantage Plan (Part C), which bundles benefits and is offered by private insurers.

Once you know your enrollment window, the next decision is foundational: do you want Original Medicare or a Medicare Advantage plan? Both paths have genuine advantages. The right answer depends on your situation, not on which plan has the flashiest TV commercial.

Original Medicare gives you broad access. You can see any doctor or specialist who accepts Medicare, anywhere in the country, without a referral. Medicare Advantage plans (Part C) often come with $0 premiums and extra perks like dental or vision coverage. But be careful to read the fine print because the majority of these "Extra Benefits" are broken down by Quarter (Instead of $1,000 in Dental Benefits, you get $250 Per Quarter). And most unused amounts are not rolled over. Additionally, oftentimes, major items are not covered at all.

A few more things related to Medicare Advantage plans:

Typically, you are only covered for services in the County you live in. If you are outside your county of residence, you can receive covered Emergency treatment only in a hospital, emergency room, or urgent care facility.

The National Average for the Maximum Out-of-Pocket (MOOP) Expense you can pay is $5,600 in 2026.

HMO plans require you to see your chosen PCP to get a referral to a specialist.

Most Medicare Advantage plans require you to use a specific network of providers and may require prior authorizations for certain services. So if you want Medicare Advantage, and you want to keep your current doctors, you need to verify that they are associated with any Medicare Advantage plan you are considering.

Most Medicare Advantage HMO Plans have a $0 Premium. However, you still pay your monthly Part B Premium of $202.90 each month, and you are responsible for all Co-Pays and Co-Insurance stated by your plan in their Evidence of Coverage rules. An MRI or CT Scan averages $400, and Hospital Stays require a per-day co-pay of $350-$450 on average.

Most Hospitals accept Medicare Advantage, but be warned that most teaching Hospitals (Mayo Clinic, Barrow Neurological Center, Johns Hopkins, Cedars-Sinai, and many other prestigious hospitals) do not accept any Medicare Advantage plans.

MEDICARE PART A

Medicare Part A covers inpatient hospital stays, skilled nursing facility care after a qualifying hospital stay, hospice care, and some home health services. Most people qualify for premium-free Part A because they (or their spouse) worked and paid Medicare taxes for at least 40 quarters, roughly 10 years.

The Part A Deductible in 2026 is $1,736 per benefit period. That applies each time you’re admitted to a hospital, not once per year, an important distinction that catches many new beneficiaries off guard. A benefit period ends once you have been discharged and have not returned to the hospital for a period of 60 days.

MEDICARE PART B

Part B covers outpatient services: doctor visits, lab work, preventive screenings, mental health services, durable medical equipment, and some home health care.

The Medicare Part B Annual Deductible for 2026 is just $283. That is how much you have to pay out-of-pocket before Medicare and your Medicare Supplement plan start to pay for your covered Expenses. Original Medicare Pays 80% of all covered costs once you have met your deductible for the year, and most of the popular Medicare Supplement/Medigap plans pay the other 20%.

If you’re already collecting Social Security, your Part B premium is automatically deducted from your monthly benefit. It is very important that you are crystal clear regarding how deductibles, copays, and coinsurance work, so you have an accurate understanding of your total Healthcare Costs, not just your premiums.

If you’re already collecting Social Security, your Part B premium is automatically deducted from your monthly benefit. Understanding how deductibles, copays, and coinsurance layer together helps you estimate your true annual costs, not just your premium.

Understanding Medicare Part C (Medicare Advantage Plans)

Medicare Advantage plans bundle Parts A, B, and usually D into a single plan offered by a private insurer. Many include vision, dental, and hearing benefits that Original Medicare doesn’t cover.

In 2026, the maximum out-of-pocket cap for Medicare Advantage plans is $9,250 for In-Network Expenses, which provides a ceiling on your annual exposure.

#3 MEDICARE PART D PRESCRIPTION DRUG COVERAGE)

Be sure to enroll in a Medicare Part D prescription drug plan when you’re first eligible to avoid permanent late enrollment penalties, even if you don’t currently take many medications. The rule is you must enroll in a plan within 63 days of your Medicare Part B Effective Date. (Most markets have at least one $0 premium Part D plan in each market.

Even if you don’t take many prescriptions right now, enrolling in a Part D plan when you’re first eligible is a smart move. Skipping it and signing up later triggers a late enrollment penalty, calculated as 1% of the national base beneficiary premium for each month you went without creditable coverage. That penalty also stays for life.

The 2026 average Part D premium is around $34.50 per month, and the maximum deductible is $615. Plans vary widely in what drugs they cover and at what tier, so checking each plan’s formulary against your specific medications is essential before choosing.

In 2026, once your out-of-pocket drug costs reach $2,100, you enter the catastrophic phase, and your cost-sharing drops significantly. This change, made permanent in recent years, provides meaningful protection for people with high-cost medications.

If your income is limited, the Extra Help program (also called the Low-Income Subsidy) can dramatically reduce your Part D costs. The 2026 Extra Help Income Limit (Individual) is $24,180.

#4 EVALUATE YOUR MEDICARE SUPPLEMENT/MEDIGAP INSURANCE COVERAGE OPTIONS

Medicare Supplement Plans and Medigap Plans are the same thing. Medigap plans (Medicare Supplement Insurance) help cover out-of-pocket costs such as deductibles, copayments, and coinsurance that Original Medicare doesn’t cover.

Original Medicare is an 80/20 Healthcare plan, where Medicare covers 80% of all covered and approved services, leaving you to pay the remaining 20%. And since there are no annual maximums with Medicare, if you get hit with a serious health issue, that 20% can be a BIG number. Heck, 20% for a Hip Replacement is about $8,000 now. This is where your Medigap or Medicare Supplement plan comes in and often pays your 20% share (Plan F, Plan G, and Plan N, HDF, HDG), depending on which Medicare Supplement plan you choose.

The most critical window is your 6-month Medigap Open Enrollment Period. It begins the month you turn 65 and are enrolled in Part B. During this window, insurers must sell you any plan they offer at standard rates, regardless of your health history. Pre-existing conditions cannot be used against you.

Plan G is currently the most popular choice; it covers virtually everything except the Part B deductible ($283 in 2026), providing broad protection with predictable costs. Plan N offers lower premiums in exchange for small copays on some office visits and a potential exposure to Part B excess charges. Plan F is the most comprehensive, covering even the Part B deductible, but it’s only available to those who were eligible for Medicare before January 1, 2020.

When comparing these plans, remember that the benefits are standardized by federal law; a Plan G from one insurer covers the same things as a Plan G from another. The only difference is the premium. Comparing prices is straightforward once you know which plan letter fits your needs.

#5 UNDERSTANDING YOUR CURRENT EMPLOYER GROUP HEALTH PLAN, COBRA, AND SEPs (SPECIAL ENROLLMENT PERIODS)

You may be able to delay Medicare enrollment without penalty if you have active employer coverage, but COBRA and retiree benefits do not qualify as creditable alternatives to Medicare.

If you choose to work past 65, or are covered through a spouse’s employer plan? You may have more flexibility than you think. Federal rules allow you to delay Part B enrollment without penalty if you have active coverage through a current employer with 20 or more employees. The keyword is “active” retiree health coverage, and COBRA does not count as a creditable alternative to Medicare.

When your employer coverage ends, you receive a Special Enrollment Period (SEP), generally 8 months to sign up for Part A and Part B without a late penalty. However, you typically have only 63 days to enroll in a standalone Part D plan or Medigap without complications.

COBRA is a common source of confusion. The majority of new Medicare Beneficiaries assume COBRA protects them from Medicare late penalties. It does not. If you’re eligible for Medicare and choose COBRA instead, Medicare becomes primary when you eventually enroll, and the months you spent on COBRA after becoming Medicare-eligible may still count against you for penalty purposes. Getting clarity on this before making a COBRA decision can prevent costly mistakes.

#6 UNDERSTANDING IRMAAA

Beyond standard premiums, you may face higher costs due to Income-Related Monthly Adjustment Amounts (IRMAA) if your income is above certain thresholds, or you might qualify for Medicare Savings Programs if your income is limited.

The $202.90 Part B premium is the standard rate, but not everyone pays it. If your income from two years ago exceeded certain thresholds, you’ll owe an Income-Related Monthly Adjustment Amount, known as IRMAA. For 2026, IRMAA is based on your 2024 tax return.

Individual filers with income above $109,000 enter the first IRMAA tier. At the highest income level (over $500,000 for individuals), the total Part B premium is $689.90 per month. Part D also carries IRMAA surcharges ranging from $14.50 to $91.

If your income has dropped significantly since that look-back year, due to retirement, the death of a spouse, or other life changes, you can appeal IRMAA using IRS Form SSA-44. The Social Security Administration can use more recent income data to recalculate your surcharge.

On the other end of the spectrum, Medicare Savings Programs help lower-income beneficiaries with premiums, deductibles, and cost-sharing. These programs are administered at the state level and have their own income and resource limits. If you think you might qualify, contacting your state Medicaid office is the right place to start.

#7 YOUR ANNUAL REVIEW DURING MEDICARE ANNUAL ENROLLMENT PERIOD

Your first enrollment is a major milestone, but Medicare isn’t a set-it-and-forget-it decision. Plans change their premiums, formularies, and networks every year. A plan that worked well this year may cost more or cover fewer of your drugs next October.

The Annual Enrollment Period (AEP) runs from October 15 to December 7 each year. During this window, you can switch Medicare Advantage plans, move from Medicare Advantage back to Original Medicare, or change your Part D drug plan. Changes take effect January 1.

Review your Medicare coverage annually during the Annual Enrollment Period (AEP) from October 15 to December 7 to ensure your plan still meets your needs and budget for the upcoming year.

Each fall, your plan sends an Annual Notice of Change letter. Read it carefully before AEP opens. If your drug costs have increased, your doctor left the network, or your premium jumped, that’s your signal to shop for alternatives. Even a 30-minute comparison during AEP can save meaningful money over the course of the year.

Your health needs also evolve. A plan that was right at 65 may not be right at 70 or 75. Building in an annual review, ideally with a licensed Medicare agent who can compare options in your area, keeps your coverage aligned with your actual life.

FREQUENTLY ASKED QUESTIONS ABOUT THIS ENROLLING IN MEDICARE CHECKLIST

What is the most important deadline to remember when turning 65 for Medicare?

Your Initial Enrollment Period, the 7-month window surrounding your 65th birthday, is the most critical deadline. Missing it can result in permanent late enrollment penalties on your Part B and Part D premiums, and those surcharges follow you for the rest of your coverage.

Can I delay enrolling in Medicare if I have employer health coverage?

Yes, but only if you have active coverage through a current employer with at least 20 employees. Retiree coverage and COBRA do not qualify as creditable alternatives, so relying on either of those to delay Medicare can expose you to penalties when you eventually enroll.

What happens if I miss my Initial Enrollment Period for Medicare Part B?

You’ll face a late enrollment penalty of 10% added to your Part B premium for every 12-month period you went without coverage. With the 2026 standard Part B premium at $202.90 per month, even a one-year gap adds a permanent surcharge. You’d also need to wait for the General Enrollment Period (January 1 – March 31) to sign up, with coverage starting July 1.

How do I choose between Original Medicare and a Medicare Advantage Plan?

Start by listing your current doctors and prescriptions, then check whether they’re covered under each option. Original Medicare offers broader nationwide provider access, while Medicare Advantage often offers lower upfront costs and additional benefits within a defined network. Your health status, travel habits, and financial situation should all factor into that comparison.

What is IRMAA, and how does it affect my Medicare premiums?

IRMAA is an income-based surcharge added to your Part B and Part D premiums. It’s calculated using your tax return from two years prior, in 2026, which means your 2024 income. Individual filers earning more than $109,000 pay higher premiums, with Part B surcharges up to $689.90 per month in the highest income bracket.

When can I change my Medicare plan after my initial enrollment?

The primary window is the Annual Enrollment Period (October 15 – December 7), where you can switch Medicare Advantage or Part D plans for the following year. Certain life events, such as moving, losing employer coverage, or qualifying for Medicaid, can also trigger a Special Enrollment Period outside AEP.

WRAPPING THINGS UP

We hope you found this article helpful and informative regarding how you can successfully navigate the Medicare Enrollment process. Working through this Medicare enrollment checklist before your 65th birthday puts you ahead of the curve, sets you up for success, and puts you in control of all of the critical decisions you will soon be making.

Perhaps the most important thing to remember is that the deadlines discussed in this article are real, and the penalties are permanent. Acting within your Initial Enrollment Period, locking in your Medigap rights while you still have guaranteed issue protection, and enrolling in Part D before any late-penalty clock starts, those three actions alone protect you from the most common and costly mistakes new beneficiaries make.

Every situation is a little different. If you’re still working, married to someone with employer coverage, or coordinating with VA benefits, your path through this checklist has nuances that a general guide can only partially address. We always think the best thing anyone approaching 65 can do is work with a local, experienced, independent Medicare Broker.

Speaking with a licensed Medicare broker who can review 2026 Medicare costs and compare plans available in your zip code provides personalized clarity that no article can fully replace. If you are not sure where to look or how to proceed, please feel free to reach out to me via email at mike@bradenmsi.com or call me directly on my cell at (480) 225-1393.

Use this checklist as your starting point. Then take the next step toward coverage that actually fits your life, your lifestyle, and please include a Son, Daughter, Niece, or Nephew to assist you.