_AZ_Initial.png)

THE MOST COMMON MEDICARE QUESTIONS IN 2026

- Michael Braden

- Feb 27

- 14 min read

Michael T. Braden January 13, 2026 Medicare 101

It is common to have many Medicare-related questions running through your mind at any given time. However, finding answers to these Medicare questions may be more complex than expected. We get it, this is the driving force behind our mission and passion to educate and serve our clients. We've worked hard to provide everyone with this great guide to get you set up for success as you begin your Medicare Journey.

This Medicare Q&A article is rather lengthy, but we believe it is worth the read.

In today's article, we wanted to provide you with the top questions we are asked by people approaching Medicare and those already enrolled in Medicare. Our goal is to help individuals by providing answers to the most frequently asked questions, so you are more informed and have more confidence in gathering Medicare information and in your Medicare Enrollment.

MOST COMMONLY ASKED QUESTIONS ABOUT MEDICARE

WHO IS ELIGIBLE TO APPLY FOR MEDICARE?

To be eligible for Original Medicare, you must be a permanent legal resident (green card holder) or an American citizen who has lived in the United States for at least five years, and one of the following:

Age 65 or older

Under age 65 and receiving Social Security Disability Income for 24 months

Diagnosed with End-Stage Renal Disease or Amyotrophic Lateral Sclerosis

To enroll in Original Medicare, you may be required to reach out to your local Social Security office in some circumstances.

IS MEDICARE FREE?

For most, the Medicare Part A premium is $0 per month. However, if you do not qualify for zero-premium Part A, the premium can be as high as $565 in 2026. To qualify for zero premium, you must have worked at least 40 quarters (10 Years) paying Medicare taxes. If you did not meet this qualification, you would be required to pay the Medicare Part A premium.

The standard Medicare Part B premium is $202.90 in 2026. This can increase based on income. This difference in premium reflects your Income Related Monthly Adjustment Amount (IRMAA). For example, if you and your spouse make $230,000 combined, you will each pay $244.60 per month in 2026. If you are subject to IRMAA, you will receive a determination letter from the Social Security Administration with your new monthly premium.

DOES THE GOVERNMENT AUTOMATICALLY ENROLL EVERYONE IN MEDICARE?

You will automatically be enrolled in Medicare at age 65 if you are receiving Social Security benefits or railroad retirement board benefits at least four months before you enroll in Medicare.

However, suppose you are not receiving Social Security or Railroad Retirement Board benefits. In that case, you will need to contact your local Social Security office to enroll in Medicare up to three months before your 65th birthday.

If you must contact your local Social Security office, you can sign up for Part A and Part B at the same time. Once you complete the application and provide the required documentation, you will begin receiving benefits on the first day of your 65th birth month.

WHAT DO I DO IF I PLAN ON WORKING PAST AGE 65?

While it is not mandatory, we recommend enrolling in Medicare Part A as soon as you become eligible if you qualify for premium-free Part A coverage. However, if you delay Medicare Part A, you will be able to enroll later during the Initial Enrollment Period (IEP) or a Special Enrollment Period (SEP) if you qualify. If you delay your initial enrollment into Medicare, you will be required to pay late enrollment penalties if you have not been covered under a Group Health Insurance Plan from an employer with more than 20 employees.

If your employer offers creditable health coverage, you do not need to enroll in Medicare Part B if you are working past age 65. Creditable coverage is healthcare coverage that provides at least equal benefits to Original Medicare. Suppose you do not have creditable coverage and do not enroll in Medicare Part B when you first become eligible. In that case, you may have to pay the Medicare Part B late enrollment penalty as long as you have Medicare Part B.

Remember that even if you have creditable coverage, it is essential to compare your current plan to Original Medicare with a Medigap plan and Part D. Often, combining these Medicare plans will provide you with the most comprehensive coverage possible.

Are Medicare Supplement and Medicare Advantage the same thing?

Medicare Supplement plans and Medicare Advantage plans are not the same thing. While both Medicare Supplement and Medicare Advantage plans bring additional benefits to Original Medicare, they work very differently.

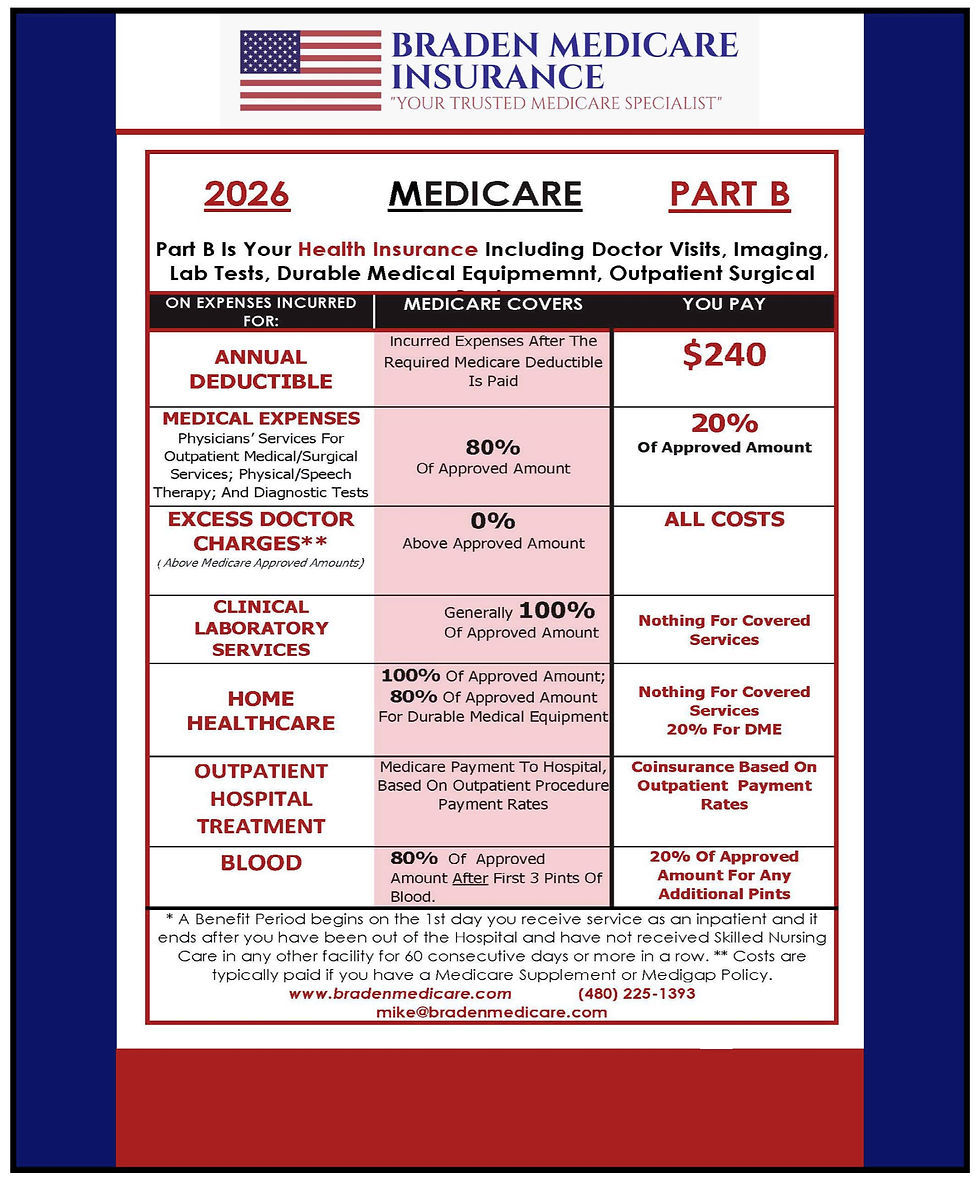

Original Medicare Covers Medicare Parts A (In-Patient Hospital Coverage) and Medicare Part B (Outpatient Health Care costs. Original Medicare is an 80/20 Health Plan, with Medicare covering 80% of all Medically Necessary services, and you are responsible for the remaining 20%. That is where the option of purchasing a Medicare Supplement comes in. Medicare Supplement plans, or Medigap plans as many refer to them, are designed to work hand-in-hand with Medicare to fill the gaps Original/Traditional Medicare does not cover.

There are 10 Medicare Supplement plans available, and these plans are standardized, meaning that each lettered Medicare Supplement plan has the same benefits in all 50 states. These plans are secondary to Medicare. Medicare Supplement (Medigap) plans pay after Medicare has paid its share. Medicare Supplement plans are the best way to have predictable costs, unmatched coverage, and convenience. In fact, for those who choose Original Medicare and A Medigap Plan G, it is the best Healthcare Coverage and best value you have ever had for comprehensive Health Insurance.

Medicare Supplements have no networks, so you are free to see any provider and receive care at any hospital that accepts Medicare Assignment (Medicare's Fee Schedule). About 93.6% of all doctors accept Medicare nationwide. The main ones who do not are Pediatricians, Psychologists, Psychiatrists, Naturopathic doctors, and Homeopathic doctors.

Medicare Advantage plans, also known as Medicare Part C, on the other hand, become your primary coverage over Original Medicare. They often require you to follow a strict network of doctors and have higher out-of-pocket costs. However, everyone needs to understand that the majority of all Medicare Advantage plans only cover you in the county you live in. You can use Emergency Rooms or Urgent Care if you are traveling, but if you see a doctor or are admitted, you will likely pay Out-Of-Network costs for care. Medicare Advantage plans also have a 20% Co-Insurance for Chemotherapy and Radiation treatments.

These additional benefits provided by Medicare Advantage plans often include dental, vision, hearing, and prescription drug coverage, as well as transportation assistance and gym memberships. However, not every plan or every carrier is required to offer these additional benefits. Additionally, with any Medicare Advantage plan, you need to read the fine print (the Explanation of Benefits). Because a plan may offer $1,000 in Dental Benefits, and you think that's good, but what they do not tell you is that they automatically break that down to $250 Per Quarter, and if you do not use these quarterly amounts, they usually will not roll over to the next quarter.

IF I CHOOSE TO DELAY MY ENROLLMENT WHEN I TURN 65, HOW DO I ENROLL LATER?

If you delayed Medicare coverage past age 65 with creditable coverage, you would need to contact Social Security to enroll in Original Medicare. The easiest way to do this is to enroll in Medicare using the Social Security Website at www.ssa.gov. Follow the Medicare Tab in the second column at the top of the homepage to enroll in Medicare.

Since you have creditable coverage, you will receive a Special Enrollment Period to enroll in Medicare Part A and Medicare Part B benefits. From there, you can enroll in a Medicare Part D prescription drug plan and Medicare Part C or Medicare Supplement. However, if you delayed Medicare coverage without having creditable coverage, you would need to enroll in Original Medicare during the General Enrollment Period. This is an annual period that runs from January 1 to March 31. Remember, coverage does not begin until July 1 when you enroll during the General Enrollment Period.

IS MEDICARE FREE?

No, unfortunately, Medicare is not free for most beneficiaries. Some people who qualify for both Medicare and Medicaid (Dual Eligible Beneficiaries) may receive extra help in paying their Medicare premiums.

Approximately 99% of all Beneficiaries do not pay for Medicare Part A.

Everyone Must Be Enrolled in Medicare Part B to access their VA Benefits (CHAMP, VA Benefits, and TRICARE).

You must be enrolled in Medicare Part B to enroll in any Medicare Advantage plan.

You must be enrolled in both Medicare Part A and Medicare Part B if you decide that Original Medicare is the right option for you and your family.

For most, the Medicare Part A premium is $0 per month. However, if you do not qualify for zero-premium Part A, the premium can be as high as $518 in 2025 or $565 in 2026. To qualify for zero premium, you must have worked at least 40 quarters or ten years paying Medicare taxes. If you did not meet this qualification, you would be required to pay the Medicare Part A premium.

The standard Medicare Part B premium is $202.90 in 2026. This can increase based on income. This difference in premium reflects your Income Related Monthly Adjustment Amount (IRMAA).

For example, if you and your spouse make $230,000 combined, you will each pay $244.60 per month in 2026. If you are subject to IRMAA, you will receive a determination letter with your new monthly premium.

ARE YOU ALLOWED TO CHOOSE A MEDICARE ADVANTAGE PLAN AND STILL GET A MEDICARE SUPPLEMENT POLICY?

No, it is illegal to enroll in both a Medicare Supplement plan and a Medicare Advantage plan. If you were to enroll in both plans, neither would become your primary coverage, leading to a denial of services. This could leave you paying out of pocket for all your healthcare services, even with both coverages.

To avoid this, it is illegal for an agent to enroll you in one plan if you are already enrolled in the other and do not have a valid way out of the plan.

WILL I NEED TO RENEW MY MEDICARE EVERY YEAR?

Original Medicare coverage is automatically renewable each year you are eligible. So, it is not necessary to renew your Medicare parts each year.

Medicare Supplement plans work the same way; once you are accepted, the plan is automatically renewable as long as you continue to pay the monthly premiums. Premiums can and will increase over time, but once you have a Medicare Supplement or Medigap policy, it is yours for life, as long as your premiums are paid.

Medicare Advantage plans are different. Some plans are available year after year, meaning if you are happy with the Medicare Advantage plan you chose, you can enroll in the same plan for the following Calendar Year. However, if you want to change plans, you can choose a new plan during the Medicare Annual Enrollment Period in the Fall, and your new plan will begin on January 1st.

WHAT HAPPENS IF I RELOCATE?

If you move to a new city or state, you will need to change your address with Social Security. Because Original Medicare is a federal program, benefits are the same nationwide. So, your benefits will not change. However, if you enroll in a Medicare Supplement or Medicare Advantage plan, you may be required to choose a new plan or pay a higher (or lower) monthly premium.

ARE THERE DEDUCTIBLES WITH MEDICARE?

Medicare Part A and Medicare Part B have deductibles and costs that change annually.

For 2026, your Medicare Part A per-occurrence deductible is $1,736, with your Part B annual deductible costing $283.

You must meet these deductibles before the respective Medicare part covers its portion of the services you receive. The Medicare Part A deductible is per occurrence, meaning you could pay that cost multiple times in one year. The Medicare Part B deductible, on the other hand, is annual. Thus, you will only pay it once per calendar year. The most popular Medicare Supplement plans will pay your Medicare Part A Deductible for you, but you will always pay your Medicare Part B deductible directly. Once you have met your Part B deductible each Calendar Year, Medicare will cover the remaining 80% of all costs.

Medicare Advantage plans (Medicare Part C) often have an annual deductible that varies by plan. You will need to review your plan information to find your yearly deductible.

If you have a Medicare Prescription Drug Plan, whether it is a Stand-Alone PDP plan or if you have Prescription Drug coverage from your Medicare Advantage plan (MAPD), you may also have a separate Part D deductible. For 2026, the maximum Part D Deductible is $615, a slight increase from the year prior. However, each plan can set its own deductible.

DOES MEDICARE COVER PRESCRIPTION MEDICATIONS?

Original Medicare does not cover prescription drugs. If you wish to have coverage for prescription Medications, you will need to enroll in a Stand-Alone Medicare Part D prescription drug plan. Medicare Part D helps cover the cost of prescription medications. Most Medicare Advantage plans also provide prescription drug coverage (MAPD). If you are a veteran with VA Benefits, your VA Prescription Drug plan is considered creditable, so there is no need to have a separate Medicare Part D plan.

If you do not enroll in Medicare Part D within 63 days of your Medicare Part B effective date, you may be subject to the Medicare Part D late enrollment penalty. This penalty is for those who delay Part D benefits without creditable coverage. You will be required to pay the additional cost as long as you have Medicare Part D.

HOW CAN I CHANGE MY ADDRESS WITH MEDICARE?

To change your address with Medicare, you must contact your local Social Security office and verify your identity. From there, they can change your address on file by answering a few simple questions and providing supporting documentation. If you have multiple addresses, you must provide your permanent residence. This is determined by where you spend most of your time throughout the year.

WHAT HAPPENS IF MY MEDICARE CARD IS LOST OR STOLEN?

If your Medicare card is lost or stolen, it is essential to report it to Social Security as soon as possible.

To report a lost or stolen card and request a replacement, you can log into (or create) a My Medicare account through Medicare.gov. From there, you can print a temporary replacement card.

To receive a new card in the mail, you will need to contact Medicare at 1-800-633-4227.

HOW DO I PAY FOR MEDICARE?

There are three ways to pay for Medicare:

If you are already receiving Social Security Benefits, your Monthly Medicare Premiums will be deducted from your Monthly Social Security Disbursement.

Your initial Medicare Statement will be for 3 Months. After that, you can set up your Medicare Portal on the www.medicare.gov portal.

Set up the Medicare Easy Pay option on the Medicare website at www.medicare.gov

DOES MEDICARE PAY FOR DENTURES

Original Medicare does not cover dentures. However, some Medicare Advantage plans may provide this benefit.

If you would instead enroll in a Medicare Supplement plan or stick to Original Medicare, you can always enroll in a separate dental plan that offers coverage for dentures.

These plans are designed to work with Medicare to create full-circle benefits for you.

WILL MEDICARE PAY FOR HEARING AIDS

Original Medicare does not cover hearing aids.

However, some Medicare Advantage plans may provide this benefit. CMS does not deem hearing aids medically necessary, so the federal healthcare program does not cover them.

If you need hearing coverage but do not want to enroll in a Medicare Advantage plan, there are several options. You can enroll in a stand-alone benefits plan that allows hearing coverage to work alongside your Medicare plan.

MEDICARE WITH VA BENEFITS

You do not need to enroll in Medicare if you have VA benefits. However, if you ever receive coverage outside of the VA system, you will need medical coverage to cover these costs. Remember, if you have VA coverage and delay Medicare Part B enrollment, you will have to pay the Medicare Part B penalty if you decide to enroll in Medicare coverage later in life. Once you enroll in Medicare, it pays primary, and the VA pays secondary.

CAN MEDICARE DECLINE YOUR COVERAGE FOR HEALTH REASONS?

Original Medicare, Medicare Advantage, and Medicare Supplement plans cannot drop you based on your health status. These plans are guaranteed renewable as long as you continue to pay the monthly premiums.

Keep in mind that if you want to change plans, there may be health-related restrictions or roadblocks. Medicare Supplement plans can deny your application based on pre-existing conditions. Medicare Part D and Medicare Advantage plans do not review your health history. However, you can only apply during certain times of the year.

WHAT CAN YOU DO IF YOU ARE STRUGGLING TO MAKE YOUR MEDICARE PREMIUM PAYMENTS?

If you cannot afford your Medicare premiums, there are several assistance programs available to help cover these costs.

First, you should visit your local Medicaid office to see if you qualify. If so, Medicaid will cover your monthly premiums and provide you with extra benefits.

Additionally, several Medicare Savings Plans are available to help low-income earners. These plans help pay your Medicare premiums and out-of-pocket costs.

HOW ARE MA HMO PLANS DIFFERENT FROM MA PPO PLANS?

Medicare HMO and PPO plans are both Medicare Advantage plans. HMO plans are the most restrictive, with tight networks and require referrals to see specialists. PPO plans are more lenient and have a more comprehensive network of doctors and hospitals you can utilize. HMO plans typically cost less than PPO plans. Both types of plans have restrictions and guidelines you must follow to receive care.

IS THERE A NETWORK WITH ORIGINAL MEDICARE?

Original Medicare does not have a typical network of doctors and hospitals. Instead, doctors and hospitals can opt in or opt out of accepting Medicare. In 2026, nearly 93% of doctors and hospitals nationwide will accept Medicare.

When you enroll in a Medicare Advantage plan, you will have to follow the network of doctors who accept your plan. This is one of the downsides of enrolling in an Advantage plan. You lose the freedom to choose your care team thoroughly. However, with a Medicare Supplement plan, you can see any doctor nationwide. This is a bonus if you often travel or have dual residency.

IS ENROLLING IN MEDICARE MANDATORY?

Enrolling in Medicare coverage is not mandatory. So, you are not required to have coverage at any point. However, if you delay Medicare enrollment without creditable coverage, you may be required to pay late enrollment penalties that do not go away. Thus, it is often more cost-effective in the long run to enroll in Medicare coverage when you are first eligible.

Medicare Part A is typically zero-premium for those who qualify, and delaying Medicare Part B can result in a significant penalty if you do not have creditable coverage. The Medicare Part B penalty adds 10% to the base premium for each 12-month period you go without coverage.

CAN I CHANGE MY MEDICARE PART D PRESCRIPTION DRUG PLAN?

If you enroll in Medicare Part D, you can enroll in a new plan once per year during the Annual Enrollment Period each fall.

Medicare Part D plans do not require you to answer health questions, so you can enroll in any plan you wish during this enrollment period. Keep in mind, any changes made to your Medicare Part D plan during the Annual Enrollment Period go into effect on January 1 of the following year.

Each year, Medicare Part D plan formularies change to reflect the needs of the majority of consumers. Your plan may change how it covers your specific drugs, and your copayments and deductibles may change each year.

So, even if you are satisfied with your benefits, it is essential to review the upcoming year's changes and ensure your drugs will remain adequately covered.

SWITCHING BACK TO MEDICARE FROM A MEDICARE ADVANTAGE PLAN

If you have a Medicare Advantage plan and wish to switch to a Medicare Supplement (Medigap) plan, you may have to wait until the Annual Enrollment Period. Unlike Medicare Supplement plans, Medicare Advantage plans require you to enroll for one year unless you have a life-changing event that would allow you to leave the plan early. This means you cannot change plans whenever you wish throughout the year. Except for your first year on Medicare, Medicare Advantage plans are a 12-month term lasting from January to December.

To change your plan for the upcoming year, you will need to enroll during the Annual Enrollment Period. By doing so, you must answer underwriting health questions to enroll in a Medicare Supplement plan. This means that your application for coverage may be denied depending on your answers to the health questions.

DO MEDICARE BENEFITS CHANGE FROM YEAR TO YEAR?

Original Medicare benefits do not change each year. However, the premiums, deductibles, and covered services may change each year. New prices are generally released in October and reflect changes for the upcoming year. Also, if there is a change in covered services, you will receive notice in advance that Medicare will no longer provide coverage.

Medicare Advantage plan benefits do change every year. It is extremely important to review your plan changes each year during the Annual Enrollment Period. During this time, you do have the option to change your plan if you do not like the new changes for the year.

Any changes made during this enrollment period will be effective on January 1st of the upcoming year.

Medicare Supplement plans do not typically change yearly. However, the deductible and premium costs may differ each year.

WRAPPING THING UP

If you have additional Medicare questions or if you would like a friendly ear to talk to about anything related to Medicare, please feel free to contact me directly. At Braden Medicare Insurance Services, we genuinely love to help people, and there is never a charge for our services, our experience, or our time.

You can call or text me at (480) 225-1393, email me directly at mike@bradenmedicare.com, or fill out our Contact Page on our website at www.bradenmedicare.com.