_AZ_Initial.png)

FULL RETIREMENT AGE FOR SOCIAL SECURITY

- Michael Braden

- Dec 28, 2025

- 7 min read

Michael T. Braden December 28, 2025 SOCIAL SECURITY NEWS

Understanding what your Full Retirement Age is for Social Security is a key part of your financial goals in retirement. The Social Security full retirement age varies for everyone. And, your Social Security benefits can be affected. In this article, we hope to share information that we think could affect every Medicare beneficiary, and specifically their Social Security benefits in retirement.

If you will rely heavily on your Social Security income in retirement, it is important to know your full retirement age and how to make the most of your Social Security benefits.

We know there are many questions about your Social Security retirement age, retirement income, and Medicare benefits. Your Social Security full retirement age will vary based on the year you were born, even though your Medicare information remains the same.

FULL RETIREMENT AGE (FRA) FOR SSI BENEFITS

Full retirement age is the age at which you become eligible to receive your full Social Security benefit amount each month. Your full retirement age is dependent on the year you were born, so not everyone will be able to retire at the same age.

Because Americans are living longer and collecting more during retirement, the full retirement age has risen over the years. Previously set at 65, the full Social Security retirement age is scheduled to increase incrementally over 22 years. We understand this can be confusing, so we’ve created our full retirement age chart. Here, you can better understand where you fall with your birth year in relation to your full retirement age.

If you retire at your full retirement age, you will receive all of the Social Security benefits you are entitled to. You can decide to retire early and take your benefits before your full retirement age. However, you can face an up to 30% reduction in monetary benefits by doing so. You also have the right to delay your retirement in order to increase the amount you will receive. Each year you delay retirement until you are 70 years old will increase the amount you are entitled to.

YOUR FULL RETIREMENT AGE IF YOU WERE BORN IN 1955

If you were born in 1955, your full retirement age for Social Security is 66 years and two months. At this time, you can begin receiving Social Security benefits at your full amount.

Remember, you can claim your benefits as early as age 62, but by doing so, you’ll forfeit a portion of your income in the process. If you decide to enroll in benefits at 62, you’ll only receive 74.2% of your entitled income. You can receive 92.2% of your monthly benefits by retiring at 65.

YOUR FULL RETIREMENT AGE IF YOU WERE BORN IN 1956

66 years and four months is the full retirement age for someone born in 1956.

Although this is the full retirement age to receive 100% of your benefits, retiring at 62 will entitle you to 73.3% of your monthly benefit amount. Retiring at 65 gets you a 91.1% monthly benefit.

YOUR FULL RETIREMENT AGE IF YOU WERE BORN IN 1957

Individuals born in 1957 will meet their full retirement age requirement at 66 years and six months. If you were born in 1957, you’d receive 100% of your Social Security benefits at this time, should you retire. For those retiring at 62, you’ll receive 72.5% of your monthly benefit, and at age 65, you’re entitled to 90% of the monthly benefit amount.

YOUR FULL RETIREMENT AGE IF YOU WERE BORN IN 1958

If you were born in 1958, your full Social Security retirement age is 66 years and eight months.

If you wish to retire early, you can permanently retire at age 62, but you’ll only receive 71.7% of your monthly entitlement. If you decide to retire at 65, you’ll receive 88.9% of your monthly benefit amount.

YOUR FULL RETIREMENT AGE IF YOU WERE BORN IN 1959

If your birth year is 1959, you reach full retirement at 66 years and ten months.

Early retirement at age 62 will allow you to receive 70.8% of your monthly benefit, and at age 65, you’ll receive 87.8% of your Social Security benefits.

FULL RETIREMENT AGE FOR THOSE BORN IN 1960 AND LATER

Anyone born in 1960 or later will have a full retirement age of 67.

If you were born in 1960 specifically, you can retire at age 62 and receive 70% of your Social Security benefits. If you wish to retire at 65 years of age, you will be subject to receive 86.7% of your monthly benefits.

WHAT IS THE AVERAGE FULL RETIREMENT AGE FOR SOCIAL SECURITY?

Did you know that, as of 2022, the average retirement age in the United States is 61? However, this is an interesting trend, as the earliest you can receive Social Security benefits is at age 62. While you may not be eligible for Social Security at 61, many employees have pension plans or retirement accounts through their employers that offer a solid financial backing for an early retirement.

Everyone has a different financial outlook, and making decisions about your financial future should be done with a professional. But if you do retire before you are eligible for Social Security benefits, it’s important to plan accordingly.

WILL YOUR SOCIAL SECURITY BENEFITS INCREASE IF YOU WORK UNTIL YOUR FULL RETIREMENT AGE?

It is possible to increase the amount you receive through Social Security. Your Social Security benefits may increase if you continue working after full retirement age, but it is not guaranteed. Social Security amounts are calculated using your 35 highest earned working years. In order for your benefits to grow, you’ll have to earn enough money that is higher than the highest 35 working years you have on record. This could increase your average income, thus increasing your benefits.

We want to inform you that by continuing to work after full retirement age, you can also increase your Social Security income by extending the receipt of benefits until you turn 70. Once you turn 70, you will max out the amount you can receive for Social Security.

WHAT MAKES THE RETIREMENT AGE RISE?

Back in 1983, the Social Security program was having financial issues. Because of this, the idea of raising the retirement age came about to help sustain the program. H.R.1900 – Social Security Amendments of 1983 legislation would pass, and the Social Security Administration would maintain the program accordingly, where it still provides retirement benefits to eligible Americans today.

By raising the retirement age, the result was that more individuals contributed to the

program for a longer period, allowing the Social Security Administration to increase its pool and pay out more benefits in the future.

CAN YOU STILL ENROLL IN MEDICARE IF YOU TAKE EALY SOCIAL SECURITY BENEFITS?

Medicare eligibility does not correlate with your retirement age. This means you can receive Medicare at age 65 regardless of your retirement status. There are instances in which you may be able to qualify for Medicare before turning the age of 65 if you are disabled, but if you are simply retiring before this time, it will not make you eligible for Medicare benefits.

Although you can’t enroll early, you also don’t want to sign up for your Medicare benefits late. Doing so can cause you to pay more upfront for Original Medicare benefits due to late penalties.

Late enrollment could also trigger you to not enroll in a qualified Medicare Part D Prescription Drug plan in a timely manner. Coverage will also incur a lifetime penalty that will never end. Additionally, any Medigap coverage you wish to enroll in may require medical underwriting to obtain if you wait to enroll. So, while retiring early doesn’t affect your ability to obtain Medicare benefits, it’s still important to plan and to avoid signing up later than your 65th birthday whenever possible.

FULL RETIREMENT AGE FOR MEDICARE IS AGE 65

You can receive full Original Medicare (Medicare Part A and Part B) benefits when you turn 65 years old. While you can receive early retirement Social Security benefits at 62, you’ll still need to wait for Medicare benefits, provided you are not disabled. The same applies to enrolling in other Medicare benefits, including Medicare Supplement (Medigap) plans, Medicare Advantage (Medicare Part C), and Medicare Part D coverage. To receive any of these benefits, you must be at least 65 years old under normal circumstances.

Remember, your full retirement age depends on your birth year, and you become eligible for Medicare when you turn 65. The two are not connected.

Note: In most states, if you qualify for Medicare early, you are only permitted to enroll in a Medicare Advantage plan until you turn 65. Then, once you turn 65, you can enroll in the Medicare plan of your choice.

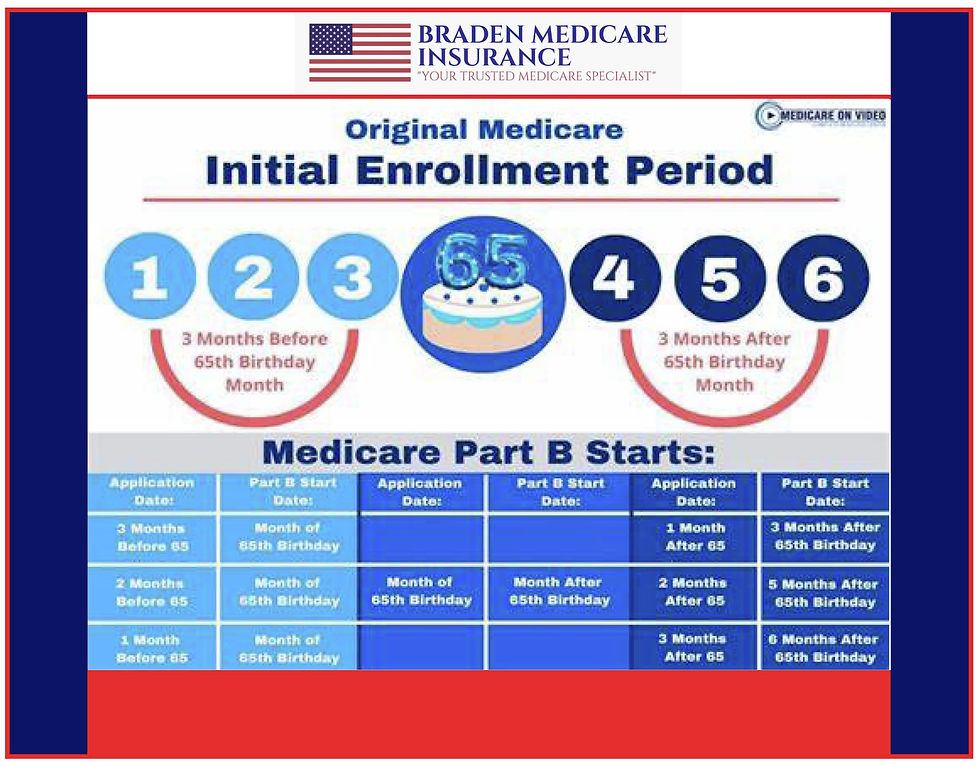

MEDICARE'S IEP (INITIAL ENROLLMENT PERIOD) FOR FRA (FULL RETIREMENT AGE)

For most, your eligibility for Medicare benefits begins three months before your 65th birthday and lasts for three months after you turn 65. This is known as your Initial Enrollment Period. This includes eligibility for Original Medicare, Medicare Supplement, Medicare Advantage, and Medicare Part D benefits.

Some may refer to this as the full Medicare retirement age, but that’s inaccurate and misleading. This is because, while both are essential benefits later in life, the retirement age affects Social Security benefits, not Medicare benefits. Therefore, regardless of your retirement status, you can receive Medicare benefits as long as you qualify and are 65 years or older.

WRAPPING THINGS UP

Preparing for your retirement means looking at multiple areas of your life. It’s an important and deserving milestone, but every decision you make matters. However, you can create a game plan that works for your lifestyle by planning ahead. To help get you started, here are some essential points to remember when planning:

Start saving money and set financial goals

Pay off as much debt as possible

Contribute to your employer’s retirement savings program,

Understand your employer’s pension plan

Explore your Social Security benefits and the age at which you wish to retire

Calculate your retirement expenses

In addition to your finances, you’ll also want to prepare for your healthcare after retirement. Many Medicare benefits are available for those turning 65, and by taking the proper steps, you can enroll in the coverage you deserve while keeping costs low.

Even if you already have Medicare benefits, reviewing your coverage from time to time is a great idea, and ensuring that you’re enrolled with the right benefits for your lifestyle. If you have any questions or just want a friendly Medicare expert to talk with, please feel free to contact us at anytime.